What We Do

Location

123 Business Street, Suite 456

New York, NY 10001, USA

Contact us

Location

Advisory services are offered by Regista Financial Strategies, LLC an investment adviser registered with the state of Colorado and in other jurisdictions where exempt from registration. Advisory services are only offered to clients or prospective clients where Regista Financial Strategies, LLC and its representatives are properly registered or exempt from registration. Investments are subject to loss and historical performance does not guarantee future performance. All information included in this document is believed to be accurate but should not be regarded as a complete analysis of any subject included. Please consult a qualified financial professional before making investment decisions.

_____

As we begin 2026, we wanted to take a moment to reflect on where we've been and share how we're thinking about the year ahead.

Before talking about expectations, it helps to briefly look back at what we just experienced.

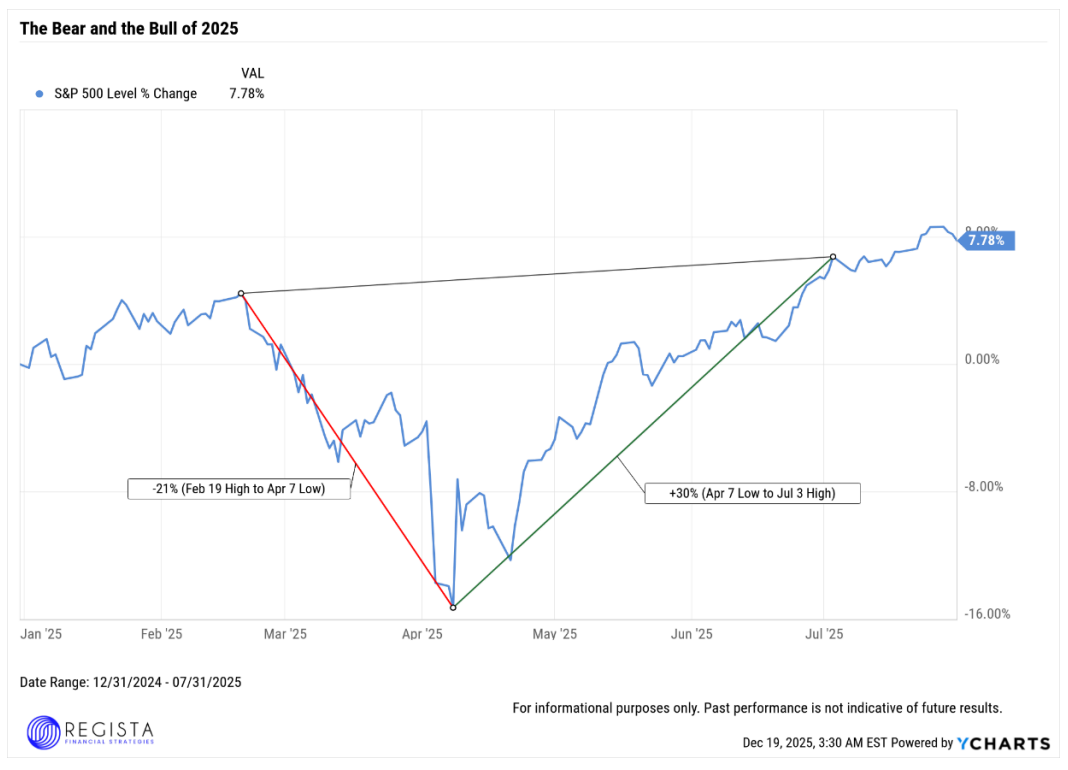

2025 was not a calm year for investors.

We saw headlines around tariffs and trade tensions, government shutdowns, new regulations for crypto assets, a surge in gold prices, and even a short bear market. April and May were especially uncomfortable, testing even well-built investment strategies.

But by mid-summer, markets recovered and moved back into positive territory, resulting in one of the fastest recoveries in history.

While that may feel surprising, it's becoming more common. News now travels instantly, emotions spread quickly, and headlines often focus on fear rather than facts. Our role as your advisory team is to filter out the noise, zoom out, and make decisions based on data, long-term trends, and realistic expectations—not daily headlines.

* The following Chart illustrates the swift reversal from bear to bull market conditions.

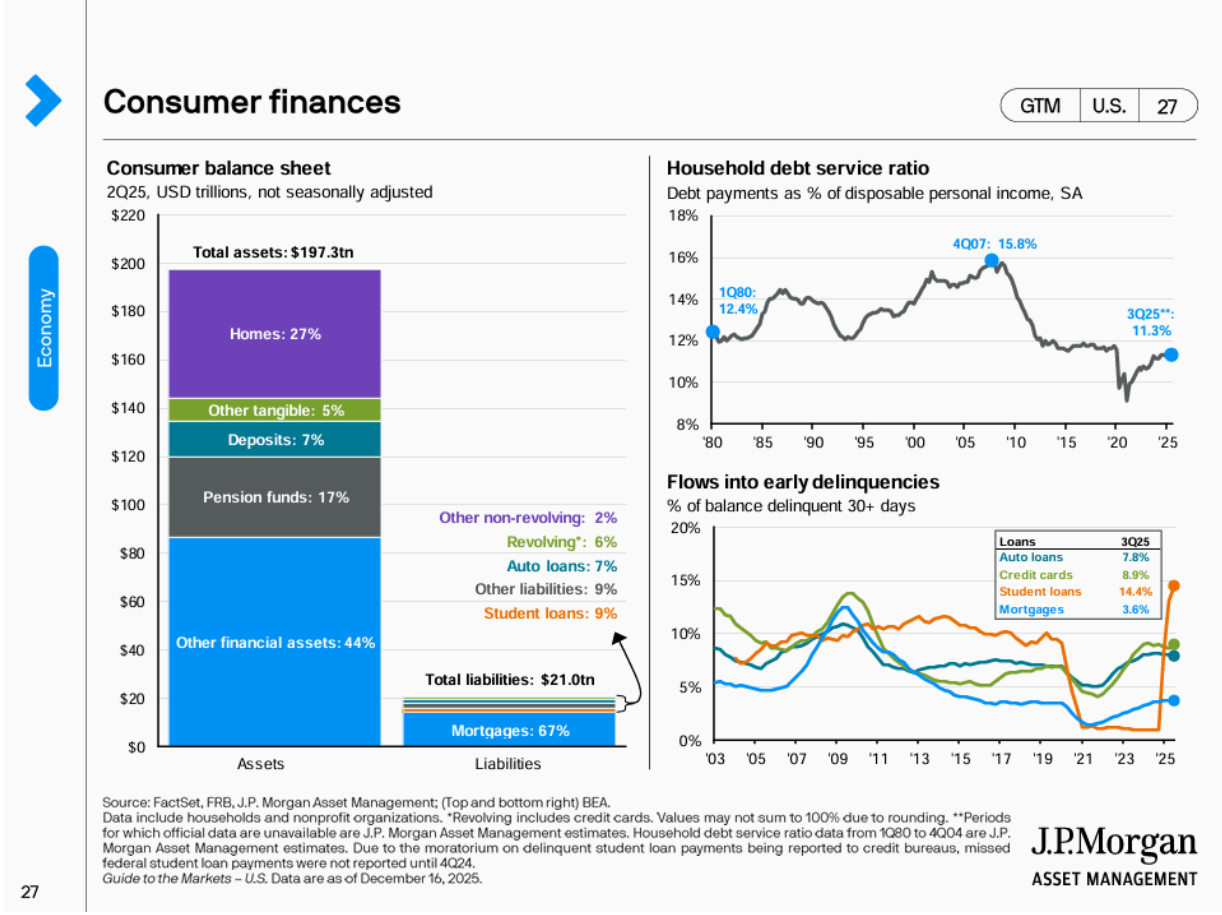

When we look at U.S. households as a whole, we see strength:

In summary, as COVID-era credit relief programs have rolled off, delinquency rates have risen but remain within historical norms—signaling a resilient consumer.

* In the following illustration you notice liabilities versus assets held by the consumer on the left. On the top right, you will notice debt service ratio at historically low levels (especially if you strip away 2020-2023). On the bottom right, the line graph depicts delinquency rates in auto, credit cards, student loans and mortgages since 2003.

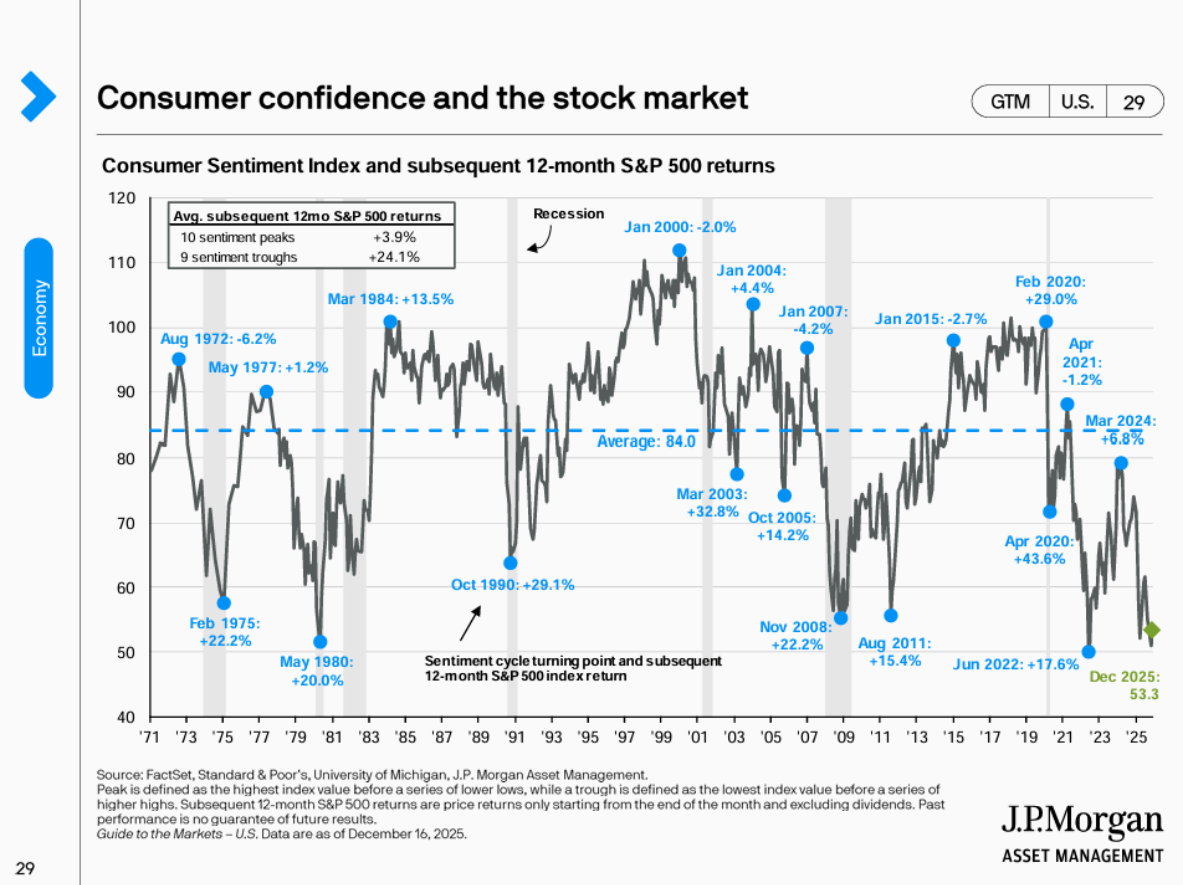

Despite the data showing resilience, many people feel pessimistic about the economy.

Historically, that disconnect matters. When sentiment is very negative, long-term market returns have often been strongest.

As Warren Buffett famously said: "Be fearful when others are greedy, and greedy when others are fearful."

*The blue dots on the following graph represent the highs and lows of consumer sentiment measures, along with the subsequent 12-month S&P 500 index returns. Currently, consumer sentiment is measuring near historic lows.

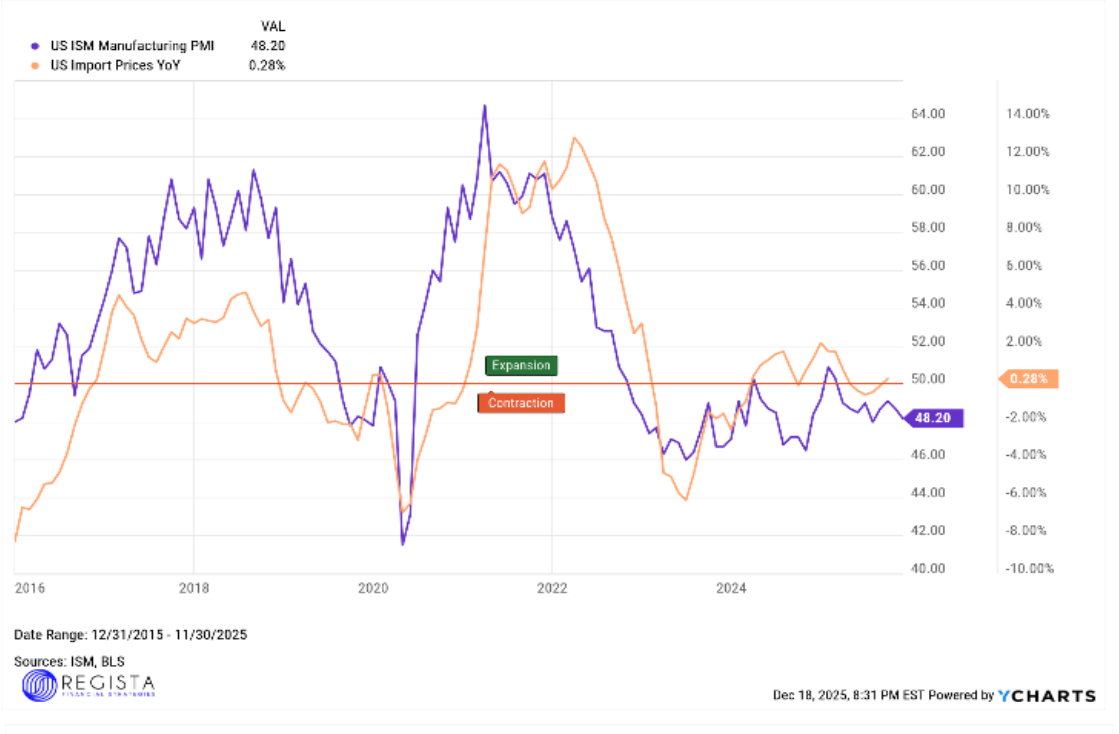

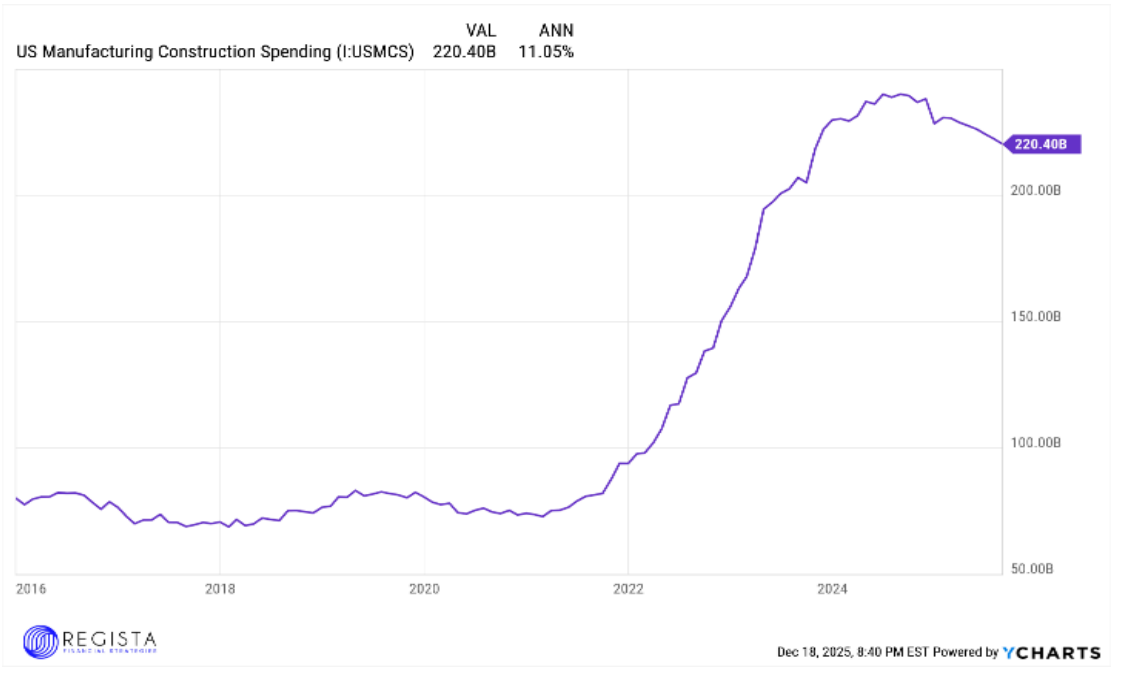

U.S. manufacturing is undergoing a significant transformation.

Trade policy changes, supply-chain reshoring, and incentives at federal and state levels are encouraging companies to build and modernize facilities in the United States. At the same time, automation and new technologies are improving efficiency—leading to increased productivity.

As a result, manufacturing construction spending is now at record levels. Construction timelines are typically two years or more, pointing to a multi-year investment cycle that supports economic growth and pulls the manufacturing sector into an expansion phase.

Why this matters: This creates long-term opportunities in areas like industrial technology, automation, energy, and infrastructure.

*The first graph highlights a sustained contraction in US manufacturing from mid-2023 through 2025. The second shows record investment in US manufacturing, positioning the sector for a return to expansion over the coming years.

The Big Picture: The U.S. economy is showing signs of achieving a "soft landing," where inflation continues to ease without triggering a major recession. Growth has slowed but remains positive, with consumer spending and job growth moderating—rather than contracting or even worse, collapsing.

At the same time, the Federal Reserve continues cutting interest rates gradually, aiming to support economic activity while keeping inflation under control.

Key Takeaway: Cooling inflation combined with steady growth and carefully managed rate cuts creates a supportive backdrop for markets. This environment improves business confidence, stabilizes financial conditions, and helps sustain earnings growth as we move into 2026.

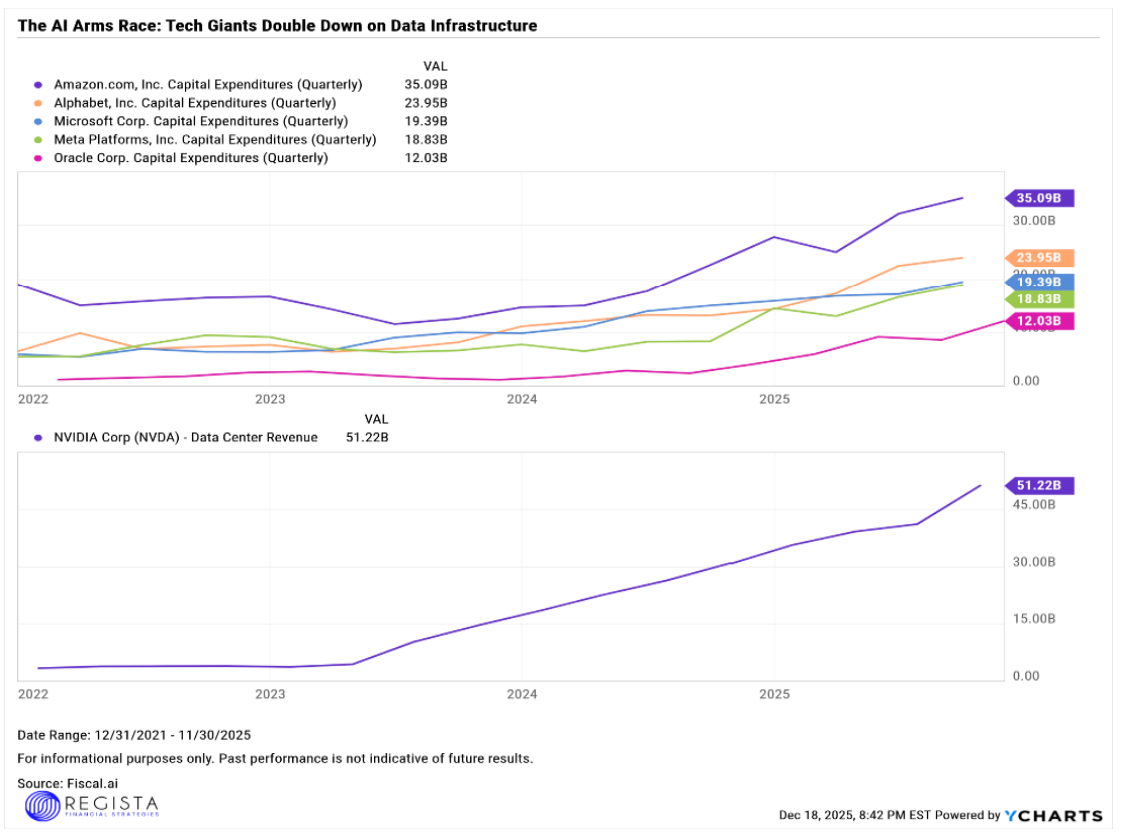

No market update would be complete without discussing artificial intelligence.

Large technology companies are spending heavily to build the infrastructure needed for AI. Collectively, five of the country's largest organizations recently invested more than $100 billion in a single quarter. This investment has driven strong performance for companies like NVIDIA and others tied to AI infrastructure.

When does spending turn into meaningful profits? AI is real and transformative—but markets will eventually want results, not just investment.

* The two graphs below show investment by the five large technology companies and the corresponding growth in NVIDIA's data center revenue driven by that spending.

Outside the U.S., countries such as Germany, Japan, and China have recently adopted policies to stimulate growth. As these economies improve, that growth has a tendency to spill over into global markets.

Markets dislike surprises. Sudden shocks tend to cause sharp, emotional reactions. Proactively understanding these risks positions us to make informed, strategic decisions should these situations materialize.

The biggest unknown is geopolitical conflict. Wars or major global tensions can disrupt trade, energy markets, and inflation expectations. Markets usually adjust over time, but the initial reaction can be volatile.

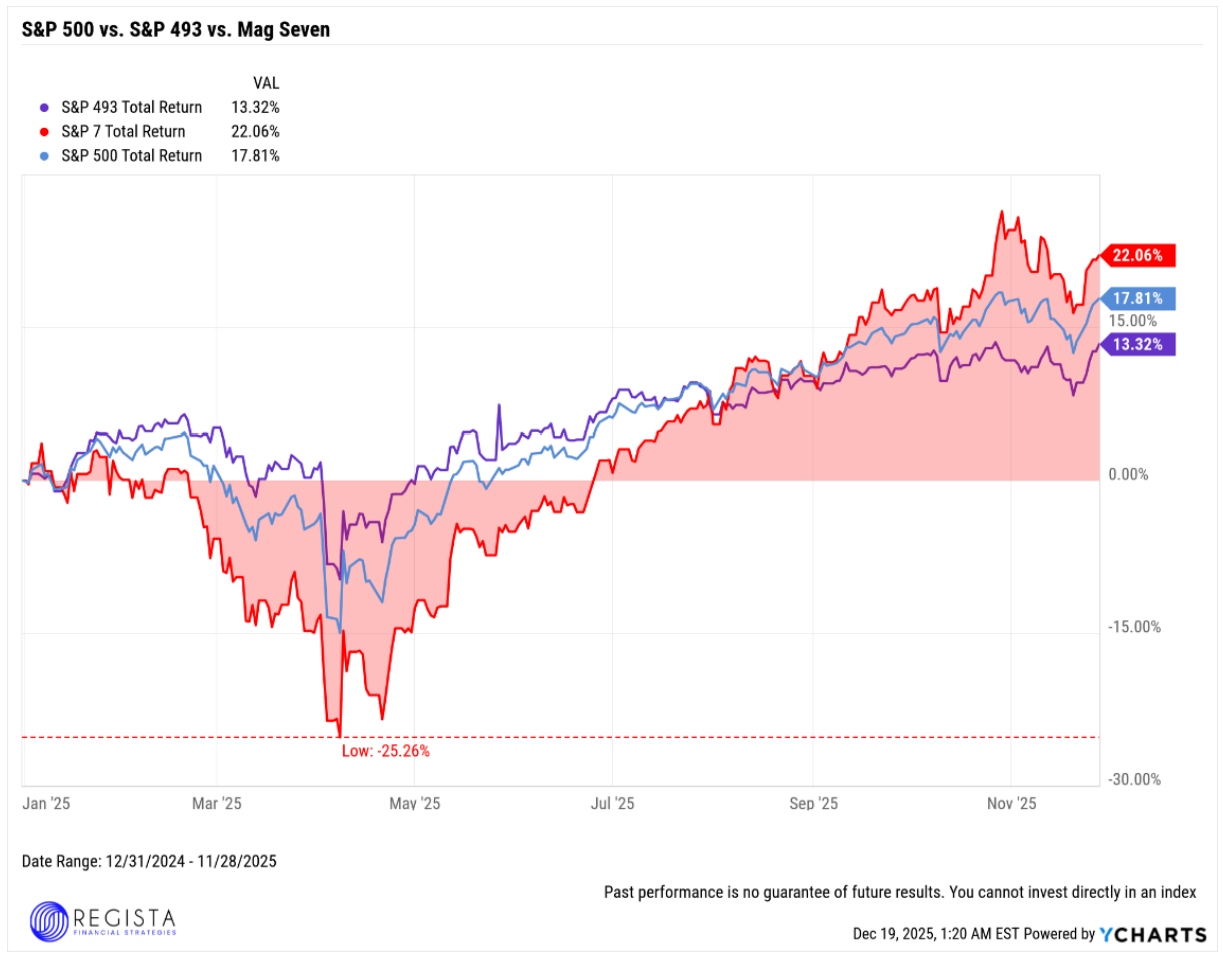

A small group of large technology companies now accounts for 47.7% (as of 12/18/25) of the S&P 500.

The so-called "Magnificent 7," accounting for nearly half of the S&P 500's market value, translates into passive investing overexposure in retail investors' accounts. Many popular index funds (especially 3 of the biggest and most popular funds, VOO, SPY, IVY) have significant exposure to just a few companies, even though they may feel like a diversified option.

This increases the risk of significant volatility if one of those companies stumbles on negative headlines.

* The following graph separates the performance of the SP500 compared to the Mag 7 and the SP500 without the Mag7 over the past year. Notice how much of the SP500 is driven by these 7 companies.

Companies have spent heavily on expansion and technology. They are now expected to move toward delivering measurable results.

Markets are watching earnings closely:

The consumer remains resilient, but cautious. Improving confidence will be key to sustaining market growth.

Here's how we're positioning our core portfolios as we move into 2026:

Markets will continue to move up and down—sometimes uncomfortably so.

Our focus remains the same:

Remember, you don't need to react to the headlines; just give us a call. That's part of our job!

As always, if you have questions or want to talk through how this impacts your personal situation, we're here for you.

I have had the privilege of working with Akram for several years, and I can confidently say that my financial journey has been nothing short of exceptional. He actively monitors your investments, ensuring they continue to align with your goals.

I can't emphasize enough how grateful I am to have Akram and Regista Financial Strategies by my side in my financial journey.

For nearly seven years, Akram has been the guiding force behind my family's financial success. His expert financial advice and meticulous planning have consistently placed us on the right path toward our goals.

We couldn't be more grateful for his expertise and support. We look forward to many more years of his invaluable guidance.

Going through a divorce after 19 years of marriage meant that finances were deeply entangled. I needed clear, sound advice on where and how to move my funds as they slowly became unknotted from my ex.

Akram was there the whole time to help me understand where everything needed to go in the smartest way possible.

Testimonials were provided by current clients of Regista Financial Strategies, LLC. Clients have not been paid for their testimonial and there are no material conflicts of interest that would affect the given testimonials. These testimonials may not be representative of the experiences of other clients, and do not provide a guarantee of future performance success and similar services.